In August 2025, mortgage rates continue to stabilize after several months of credit tensions.

This calm period creates a more favorable environment for both borrowers and sellers, with a market that is gradually regaining fluidity. In this in-depth article, discover how mortgage rates evolved in August 2025, which borrower profiles are most sought-after, expert tips for securing a loan or selling property, and what to expect this fall.

Mortgage Rate Barometer – August 2025: Key Figures to Know

August 2025 confirms a trend of mortgage rate stabilization that began several months ago. Major banks, reassured by a more predictable economic climate and the decline of 10-year government bond yields (OATs), are maintaining relatively accessible financing policies. As a result, borrowers — whether they’re first-time buyers, property investors, or seeking a primary residence — can still benefit from competitive fixed rates.

Here are the updated mortgage rate figures for August 2025, published by CAFPI on July 26. They reflect three tiers: the lowest negotiated rate, the average observed rate, and the posted benchmark rate from banking institutions.

Fixed Mortgage Rates by Loan Term (10, 15, 20, 25 years)

| Loan Term | Lowest Rate | Average Rate | Benchmark Rate |

|---|---|---|---|

| 10 years | 2.73% | 2.99% | 3.48% |

| 15 years | 2.81% | 3.06% | 3.71% |

| 20 years | 2.92% | 3.14% | 3.84% |

| 25 years | 3.05% | 3.27% | 3.98% |

Source: CAFPI

These rates apply to fixed-rate loans, which remain the preferred option for most borrowers due to their predictable repayment costs and the financial security they offer during the early years of the loan.

The best negotiated rates are reserved for borrowers with strong profiles: a significant down payment, stable employment, controlled debt levels, and sound financial management.

Analysis of Mortgage Rates in August 2025

August confirms the stabilization of interest rates following the rise observed between mid-2023 and late 2024. Although benchmark rates remain high, negotiation margins have improved since May 2025 thanks to renewed competition among banks seeking to attract new clients.

The gradual decrease in rates is particularly evident on longer loan terms (20 and 25 years), with differences exceeding 0.70 points between posted and negotiated rates. This dynamic improves borrowing capacity for households, especially in regions and cities where property prices remain accessible.

Another encouraging sign: average rates have slightly decreased compared to July, indicating a modest but real downward trend. This is good news for current real estate projects, provided the loan application is complete and well-prepared.

Variable Rates vs. Nominal Rates: What’s the Difference in 2025?

Although not widely used in France, variable-rate loans are still offered by some banks. Typically indexed to the Euribor, these loans can offer lower initial rates but come with significant fluctuation risk. In periods of monetary uncertainty or rising inflation, they are generally less attractive, especially for first-time buyers.

On the other hand, the nominal rate represents the base interest rate used to calculate the loan, excluding items such as mortgage insurance, administrative fees, and guarantees. To assess the real total cost of a loan, it’s essential to compare the APR (Annual Percentage Rate), which includes all additional fees.

Tip: To get the best rate in August 2025, compare offers from several banks with similar borrower profiles and work with a Capifrance advisor or mortgage broker.

Borrower Profiles: Who Gets the Best Mortgage Rates in August 2025?

In August 2025, banks continue to review loan applications according to strict criteria. As interest rates stabilize, lenders remain cautious and prefer applicants with strong financial profiles. This doesn’t mean only high-income borrowers get good rates — but some factors make a significant difference.

Understanding favorable borrower profiles and what banks look for is crucial to securing a loan under optimal conditions.

Preferred Borrower Profiles

First-time buyers are still welcomed, particularly if they can contribute a down payment of at least 10% of the property price. This shows an ability to save, commitment to the project, and reduces risk for the bank.

In addition to the down payment, lenders assess several key factors:

Stable employment (permanent contracts or established self-employment),

Controlled debt-to-income ratio (ideally ≤ 33%),

Responsible financial management.

These criteria significantly influence access to the best negotiated rate and determine loan conditions (duration, monthly payments, guarantees). Banks aim to attract low-risk, creditworthy clients — making the quality of your file more important than ever.

Down Payment, Guarantees, and Additional Costs: Key to Attractive Mortgage Rates

While interest rates are now relatively stable, other components of the mortgage can greatly affect the overall cost. These include:

Administrative fees,

Borrower’s insurance,

Required guarantees (such as mortgage or guarantor fees).

These are important comparison points between offers. Even with identical borrower profiles, differences in these costs can total several thousand euros over the loan term.

Also, the type of loan matters: a lower nominal rate isn’t always better if associated fees are high. That’s why some borrowers consider variable-rate loans, which may be more attractive initially but riskier over time. In a stabilization period, banks may offer both options, but fixed rates remain more reassuring to secure the early years of repayment.

Finally, it’s critical to analyze market drivers, such as:

Monetary policy decisions,

10-year government bond yields (OAT),

Geopolitical context.

These factors can influence interest rate trends in the coming months and should be part of any serious financing strategy.

Mortgage Borrowing Capacity in France: What Is the Impact of Interest Rates in August 2025?

In August 2025, French households’ borrowing capacity remains a key factor in achieving their real estate goals. While the rate stabilization observed since spring has improved visibility, it hasn’t erased regional disparities or budget constraints. Even small fluctuations in the total cost of a loan directly affect the size of the property that can be purchased — especially in large cities.

Understanding the real effect of interest rates on your budget is essential to choosing the financing solution best suited to your situation.

Calculating Borrowing Capacity Based on Interest Rate

The principle is simple: the lower the interest rate, the higher the loan amount a borrower can obtain for the same monthly payment. For example, with a monthly payment of €1,000 over 20 years:

At 3.14% (current average rate), a household can borrow around €170,000

At 2.92% (best negotiated rate), the amount rises to around €175,000

At 3.84% (benchmark rate), it drops to around €160,000

A difference of half a point in the interest rate can therefore mean up to €15,000 more (or less) in purchasing power. This differential becomes a key comparison point when evaluating multiple offers.

In this context, every borrower has an interest in negotiating not only the rate, but also administrative fees, insurance, and other credit-related costs between banking institutions.

Practical Examples: Paris, Grand Est, Pays de la Loire, and Other Regions

The impact of interest rates on buying power varies significantly depending on the region and price per square meter. Here are a few concrete illustrations:

In Paris, with an average price around €10,000/m², even gaining €10,000 in borrowing capacity often only adds 1 m² to what can be purchased.

In Grand Est, where the average price is around €2,200/m², that same gain could add 4 to 5 m².

In Pays de la Loire, a moderately growing region, the benefit could be an additional 2 to 3 m² with optimized financing.

In Auvergne-Rhône-Alpes, a slight rate improvement may make the switch from an apartment to a house in suburban areas more feasible.

In Nouvelle-Aquitaine, mid-sized cities like Niort, Bergerac, or Angoulême offer a good balance between price and area, with more noticeable leverage if loan conditions improve.

In Occitanie, in cities like Narbonne or Albi, a 0.2-point rate variation could mean up to 8 extra square meters of livable space for the same monthly budget.

These examples highlight the importance of tailoring your project to local conditions — and of being guided by professionals when assessing your borrowing power. At Capifrance, our advisors use precise simulation tools to help align your property search with your financial reality.

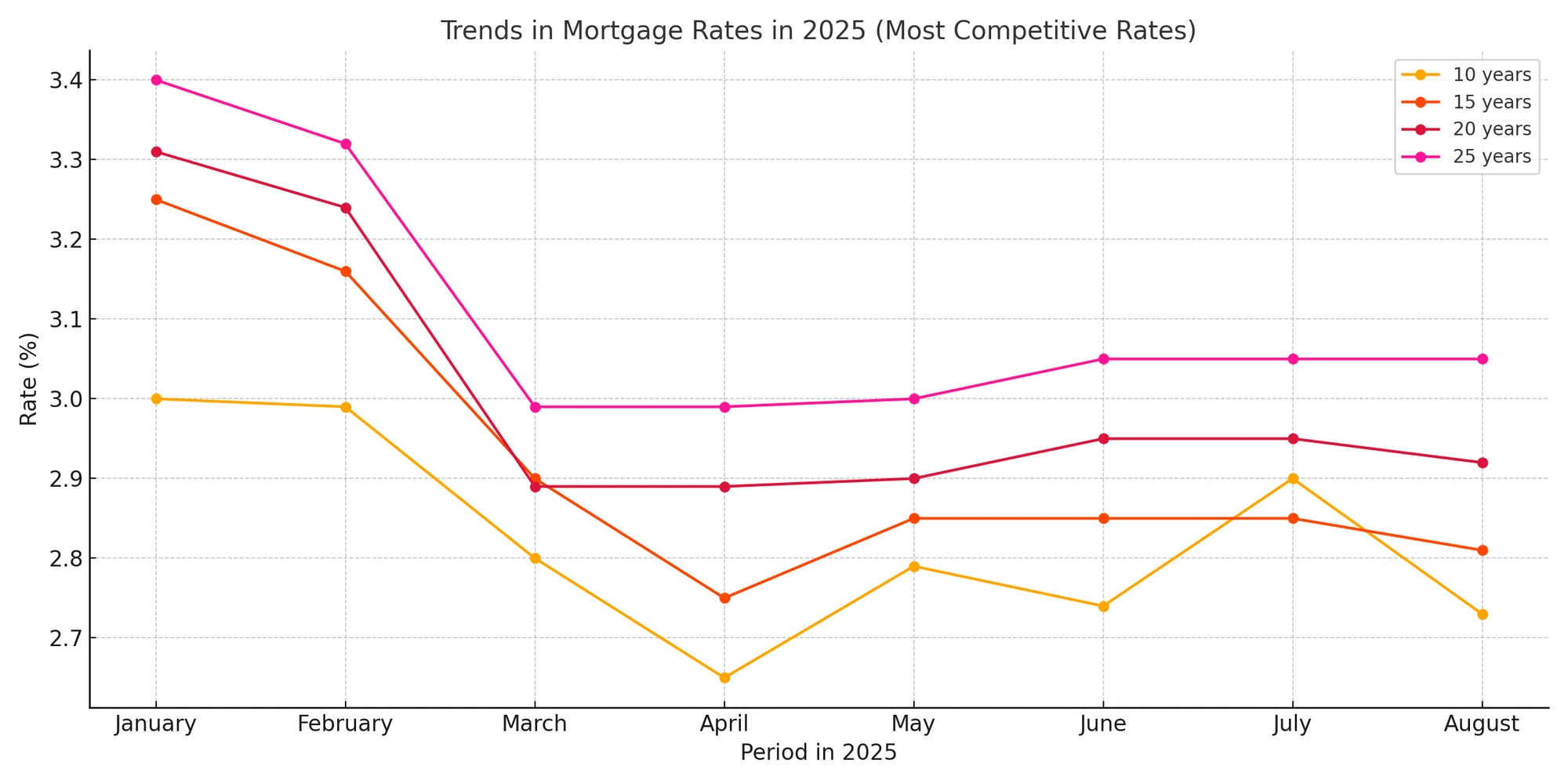

Mortgage Rate Evolution in France Since Early 2025: Stabilization or Real Decline?

| Period (2025) | 10 yrs | 15 yrs | 20 yrs | 25 yrs |

|---|---|---|---|---|

| January | 3.00% | 3.25% | 3.31% | 3.40% |

| February | 2.99% | 3.16% | 3.24% | 3.32% |

| March | 2.80% | 2.90% | 2.89% | 2.99% |

| April | 2.65% | 2.75% | 2.89% | 2.99% |

| May | 2.79% | 2.85% | 2.90% | 3.00% |

| June | 2.74% | 2.85% | 2.95% | 3.05% |

| July | 2.90% | 2.85% | 2.95% | 3.05% |

| August | 2.73% | 2.81% | 2.92% | 3.05% |

Source: CAFPI – Best negotiated rates in 2025

Between January and August 2025, the mortgage market underwent a notable shift. After a sharp rate increase in 2023 and a plateau in 2024, the first months of 2025 saw a decline followed by progressive stabilization, now confirmed again in August.

Downward Trend: What Are the Influencing Factors?

The current trend is driven by a more favorable environment for real estate financing. Among the main factors:

The drop in 10-year government bond yields (OATs), which fell below 3.20% at the end of July 2025, allowing banks to lower their benchmark rates;

Decisions by the ECB: maintaining a cautious monetary policy and holding off on rate hikes since spring has reassured lenders;

Contained and better-anticipated inflation;

Banks' willingness to revive their mortgage activity in a recovering market and attract new clients.

These combined factors have led to a gradual easing of proposed rates, with a growing gap between posted benchmarks and actually negotiated rates.

The Role of the European Central Bank and Government Bonds (OATs)

The ECB's monetary policy remains a benchmark for the market. By refusing to raise its key rates in July and August 2025, the institution sent a positive signal to banks, who in turn adjusted their rate grids accordingly.

Moreover, the 10-year OAT yield, frequently used in fixed-rate loan pricing models, has stabilized below 3.2%. This technical decline opens the door for banks to gradually lower rates in their offers, even though they remain cautious given the ongoing geopolitical uncertainties.

We now see a divergence in strategy among banks: some favor long-term loans with attractive rates to boost applications, while others focus on low-risk profiles, adjusting negotiation margins accordingly.

Capifrance Tips: Borrowing at the Right Time

Taking out a mortgage in August 2025 may be a real opportunity if you adopt the right strategy. In a market where mortgage rates are gradually declining yet still hovering around average levels, banks are becoming more responsive to attract strong borrower profiles. This makes it a good time to apply for financing—provided your file is well prepared.

Capifrance advisors are here to support you every step of the way to help you obtain the best mortgage conditions and complete your purchase or sale successfully.

Key Elements for Negotiating the Best Mortgage Rate

To secure the best rate this month, it's essential to present a solid borrower profile and highlight the reassuring elements of your application. Here are the main levers:

A personal down payment of at least 10 to 15% of the total property price (more depending on the project);

Stable employment: permanent contract, seniority in the position, steady income;

Good bank account management: regular savings, no payment incidents, no recent consumer loans;

A clear and complete file, including all supporting documents, chosen borrower insurance, and anticipated application fees;

A realistic project aligned with your resources and medium-term goals.

Tip: Banks assess each application with their own criteria, but all focus on the same fundamentals. Negotiation margins on rates, guarantees, or repayment conditions can make all the difference.

Choosing Between Fixed, Variable, Nominal, and APR Rates

There are many financing options available, but they are not all equal. It is crucial to compare proposals from multiple angles:

Nominal rate: the raw interest rate offered by the bank, excluding fees;

APR (Annual Percentage Rate): includes all additional costs (insurance, guarantees, application fees) and is the main metric to compare two loans;

Variable rate: sometimes lower at the start but riskier in an uncertain market, especially without a cap;

Fixed rate: the most commonly used, it guarantees consistent monthly payments throughout the loan term, offering maximum visibility—especially in the early years.

To determine the financing formula best suited to your profile, project, and life plans, it's best to be supported. A Capifrance advisor can guide you to the right banking partner, help you build your file, or connect you with a broker to secure the most favorable conditions.

Selling Property in a Period of Stabilized Interest Rates: Capifrance’s Advice for Property Owners

When it comes to mortgage rates, much of the focus is often on buyers—but sellers are equally affected. In August 2025, the stabilization of interest rates is gradually reviving demand, especially among first-time buyers and purchasers with significant down payments. This makes it a strategic time to sell—provided you anticipate market expectations and price your property appropriately.

Why Stable Interest Rates Are Good News for Sellers

Since late spring 2025, buyers have been gradually returning to the market. The combination of a more manageable total loan cost, wider room for negotiation, and better financing access has enabled many households to restart their property purchase projects.

For sellers, this dynamic is a real opportunity:

Buyers' borrowing capacity has increased slightly compared to July, expanding their property search;

Banks are more willing to finance solid borrower profiles, offering stronger support for well-prepared applications;

A gradual return of consumer confidence in a stabilizing economy encourages purchase decisions.

In other words, while the recovery remains cautious, it is clear—and more favorable than during the second half of 2024.

Adjusting Your Price to Match Buyers’ Financing Conditions

To sell successfully in August 2025, it’s important to consider buyers’ financing constraints. Longer loan durations, additional costs (guarantees, application fees, borrower insurance), and slight variations in interest rates depending on the applicant’s profile can all affect their total budget.

Here are some best practices:

Price your property fairly, based on local price per square meter and average buyer affordability in your area. With Capifrance, you can get a precise and professional valuation of your property;

Highlight key strengths: energy rating, low charges, quality of the environment, proximity to transport;

Be open to negotiating loan-related conditions: signing deadlines, mortgage contingency clauses, flexibility on the final sale date;

Accept that some buyers may need a few extra weeks to complete their application process or obtain loan approval.

A Capifrance advisor will support you every step of the way to position your property correctly, target the right buyers, and secure the sale quickly. They can also help if you're relocating or planning a sell-to-buy transition.

Forecast and Outlook for Mortgage Rates in Fall 2025

As summer draws to a close, many questions arise about how mortgage rates will evolve over the coming months. After several weeks of confirmed stabilization—and even some gradual reductions in negotiated rates—fall 2025 could confirm a favorable trend for borrowers.

However, these trends remain sensitive to international influences, upcoming monetary policy decisions, and banks’ capacity to sustainably resume lending.

Will Interest Rates Stabilize or Fall by the End of 2025?

Several short-term scenarios are emerging:

Optimistic scenario: a continued drop in average rates, if 10-year bond yields (OATs) stay below 3% and the European Central Bank (ECB) maintains its accommodative policy. The ECB’s upcoming decisions this fall will be key;

Cautious scenario: a prolonged stabilization around current levels, with minimal variations based on applicant profile and project type (main residence, rental, investment);

Restrictive scenario (less likely): renewed rate pressure in the event of inflation spikes or external shocks tied to geopolitical tensions.

Regardless of the scenario, fixed-rate mortgages are likely to remain the preferred option, with continued negotiation margins for strong borrower profiles.

How to Prepare for Upcoming Changes in Mortgage Conditions

For both buyers and sellers, fall is shaping up to be a strategic period. Here are a few practical tips:

Start your application process in early September to benefit from current rates before potential increases. Keep in mind that lender review times can delay project completion;

Compare APR (Annual Percentage Rate), not just the nominal rate, to get a full picture of your loan’s true cost;

Emphasize your down payment, stable employment, and all loan factors that strengthen your profile (savings, no consumer loans, employment stability);

If you're selling, adjust your sales strategy to the market’s recovery phase. A fair valuation, clear communication, and fast response times can help speed up the sale.

At Capifrance, our advisors help you bring your real estate project to life—buying or selling—with competitive financing options, aligned with your life goals and investment plans.

Conclusion: Key Takeaways on Mortgage Rates in August 2025

Average rates range from 2.99% to 3.27%, depending on loan term, with best negotiated rates improving significantly for strong profiles;

The decline in rates at the end of 2024 and their stabilization in spring 2025 is confirmed once again this August;

Stable profiles—with down payment, good financial management, and steady income—are most likely to secure sub-3% borrowing rates;

Borrowing capacity has improved slightly, breathing new life into real estate projects in many regions;

It’s a good time to borrow or sell, provided you're well advised—especially on loan structure, APR, and additional fees;

Fall 2025 could reinforce the downward trend, depending on ECB decisions, bond yield trends, and overall economic stability—so it’s wise to act while current favorable conditions remain.

Contact your local Capifrance advisor to make your purchase or sale a success, and browse our real estate listings to find the property of your dreams.

Selling to buy? Request a precise valuation to determine the right price and sell under the best conditions.

Related Articles:

News – Mortgage Rates in July 2025: Trends and Forecasts

News – Mortgage Rates in June 2025: Trends and Forecasts

News – Mortgage Rates in May 2025

News – Mortgage Rates in April 2025: Spring is Here!

News – Mortgage Rates in March 2025 Below 3%

News – Mortgage Rates in February 2025: Trends and Outlook

FAQ: Frequently Asked Questions About Mortgage Rates

What is the current mortgage rate?

In August 2025, the most competitive negotiated rates are around 2.73% for 10 years, 2.81% for 15 years, 2.92% for 20 years, and 3.05% for 25 years (source: CAFPI).

Will mortgage rates go down in 2025?

A slight decline began this summer, following the drop in 2024 and stabilization in early 2025. The trend will depend on ECB decisions, bond markets (OATs), and economic developments in the fall.

What’s the monthly payment for €140,000 over 25 years?

At a rate of 3.05% over 25 years, the monthly payment (excluding insurance) is about €670. The amount may vary depending on APR and insurance.

Which bank offers the lowest mortgage rate?

Brokers like CAFPI, partners of Capifrance, negotiate the best rates with several partner banks. No single bank always leads—it depends on the applicant's profile and file.

What interest rate can I get for a mortgage?

As of August 2025, the most competitive fixed rates in the French market range from 2.73% to 3.05%, depending on loan term and borrower profile (down payment, income, job stability, etc.).

What’s the average mortgage rate in 2025?

The average observed rate for 20-year loans since the start of the year is around 3.00%, with a downward trend beginning in the spring.

Why are mortgage rates rising?

In 2024 and 2025, the trend actually reversed: rates decreased and have remained relatively stable for several months now.

How do you calculate a mortgage rate?

The nominal rate is the base interest, but the APR (Annual Percentage Rate) includes all costs (fees, insurance, guarantees). This is the rate to compare.

How can I negotiate or renegotiate my mortgage rate?

Present a solid profile (stable income, down payment, low debt), compare offers between lenders, and work with a Capifrance advisor or broker to optimize conditions.

What is the mortgage rate over 25 years?

As of August 2025, the most competitive 25-year rate is 3.05% (CAFPI data). This may vary depending on your file and market conditions.

Author:

Frédéric Rémy – Director of Commercial Performance

A real estate professional for several years within the Capifrance network, I would like to share with you some key tips to help you succeed in your property project with the support of our advisors.