In an economic environment that remains fragile but full of opportunity, many borrowers are wondering when the right time might be to make their property purchase a reality. In July 2025, mortgage rates have reached a point of equilibrium. The stabilization phase that began in the spring is now confirmed and is supporting the market’s recovery. This article provides a detailed overview of current mortgage rates, recent trends, forecasts for the autumn, and the best strategies to secure the most competitive rates. With Capifrance, discover this summer’s mortgage rates in 2025!

Mortgage Rates in July 2025: Analysis and Comparison

July 2025 opens with a mortgage market that appears to have found a new balance. Financing conditions remain attractive for borrowers, despite ongoing economic uncertainty. The period is still favorable for a real estate purchase.

Confirmed Stabilization of Mortgage Rates in July 2025

In July 2025, mortgage rates continue the stabilization trend observed since May. After several months of continuous decline followed by a slight increase in June, the barometers show virtually unchanged levels. This lull, while fragile, is reassuring for borrowers and still allows them to take out home loans under favorable conditions.

According to data from Cafpi as of June 16, 2025, mortgage rates in July are as follows:

Loan Term | Lowest Rate | Average Rate | Standard Rate |

|---|---|---|---|

10 years | 2,90 % | 3,05 % | 3,48 % |

15 years | 2,85 % | 3,04 % | 3,71 % |

20 years | 2,95 % | 3,18 % | 3,84 % |

25 years | 3,05 % | 3,28 % | 3,98 % |

(Source: CAFPI – Observed negotiated rates)

This stability can be attributed to a temporary balance between still-tight refinancing conditions (rising government bond yields) and the European Central Bank’s ongoing accommodative monetary policy. Although banks are exercising more caution, they are maintaining competitive rates to attract strong borrower profiles. For borrowers, this means there’s still time to secure fixed rates around 3% before any potential market reversal. Planning to buy your main residence or invest in real estate? Discover our top property listings throughout France.

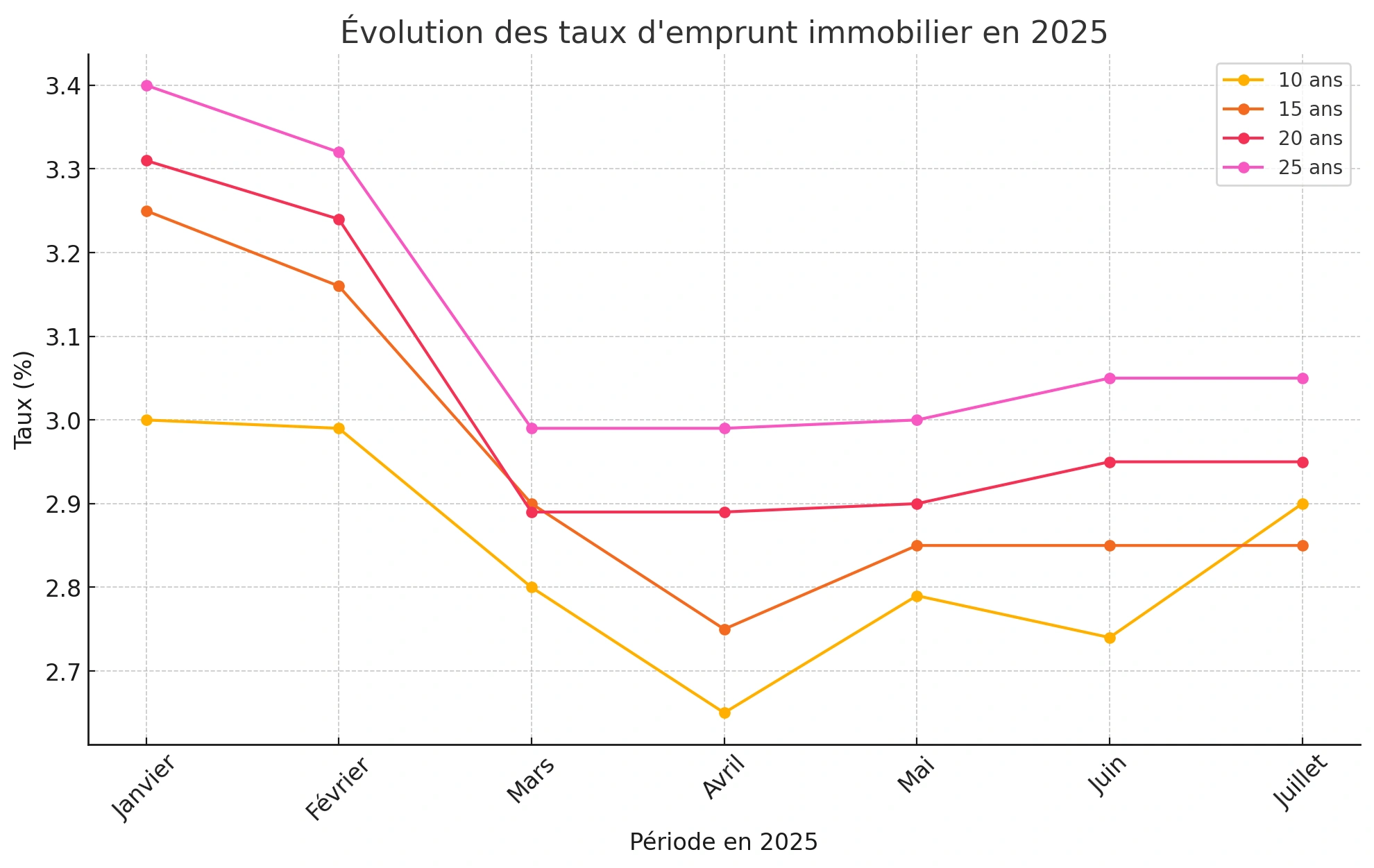

Evolution of the Most Competitive Mortgage Rates in the First Half of 2025

Over the first six months of the year, mortgage rates experienced a decline until April, followed by a gradual stabilization in May and June. Here’s how the average rates evolved:

Period in 2025 | 10 years | 15 years | 20 years | 25 years |

|---|---|---|---|---|

January | 3,00 % | 3,25 % | 3,31 % | 3,40 % |

February | 2,99 % | 3,16 % | 3,24 % | 3,32 % |

March | 2,80 % | 2,90 % | 2,89 % | 2,99 % |

April | 2,65 % | 2,75 % | 2,89 % | 2,99 % |

May | 2,79 % | 2,85 % | 2,90 % | 3,00 % |

June | 2,74 % | 2,85 % | 2,95 % | 3,05 % |

July | 2,90 % | 2,85 % | 2,95 % | 3,05 % |

(Source: CAFPI)

This trend reflects a slowdown in the rate drop that started early in 2025, with stabilization around 3% for standard 20- to 25-year terms. This provides buyers with greater visibility for planning their real estate projects while still benefiting from favorable financing conditions in summer 2025. Need help bringing your project to life? Contact your local Capifrance real estate advisor to get expert advice and full support.

Also read on the topic:

- Mortgage rates in June 2025: trends and forecasts

- Mortgage rates in May 2025

- Mortgage rates in April 2025: spring is here!

- Mortgage rates in February 2025: trends and forecasts

Economic Context of July 2025: What Impact on Mortgage Rates?

In July 2025, mortgage rates are being shaped by several key macroeconomic factors. The environment is still influenced by an accommodative monetary policy, tense bond markets, and growing geopolitical uncertainty. Understanding these dynamics is essential to anticipate trends and optimize your property purchase.

Banks are adjusting their rate sheets based on the broader economic context: they weigh the effects of ECB policy and the trajectory of the 10-year OAT (French government bonds), while remaining cautious in the face of inflation and international tensions. As a result, the rate stability or slight increase observed in July reflects a complex balancing act between banking margins and attractiveness for borrowers.

Inflation, 10-Year OAT, and Economic Conditions: Mortgage Rates Under Pressure

The rise of the 10-year OAT to around 3.20% in June is a key concern for banks, as it signals their own refinancing costs. The higher this rate climbs, the more likely mortgage rates will increase in turn, in order to preserve financial margins. Meanwhile, inflation in the eurozone, even if moderate, weighs on banking forecasts, pushing lenders to adjust their credit grids for the month to account for these economic pressures.

ECB Monetary Policy: Will the 8th Key Rate Cut Positively Impact Mortgage Rates?

In mid-June 2025, the European Central Bank lowered its key rates from 2.25% to 2%, marking the eighth reduction since last summer. This move aims to support growth and ease household budgets by improving access to credit. However, this mechanism isn’t instantaneous: the rate cut doesn’t immediately translate into lower mortgage rates, which also depend on the volatility of government bonds. Still, this environment offers a degree of stability, limiting the risk of rate hikes in the coming months and perhaps even paving the way for another decrease.

How to Get the Best Mortgage Rates in July 2025?

Depending on borrower profiles and financial guarantees, some buyers can access below-average mortgage rates, while others are offered more standard conditions. By understanding what banks are looking for, you can improve your chances of securing a favorable rate and increasing your borrowing capacity.

The most attractive conditions are generally granted to borrowers who offer the highest level of security for the bank: a stable job, a substantial down payment, impeccable financial management, and ideally a well-secured project.

Borrower Profiles Favored by Banks in July 2025

To obtain rates below the average, banks prefer reassuring profiles: permanent employment contracts (CDI) outside the trial period, stable and sufficient income, and a personal contribution of at least 10 to 20% of the loan amount. Having residual savings (equivalent to about one year of monthly payments) further increases the bank’s confidence. Young first-time buyers with a modest down payment but strong future potential also have an advantage: some banks offer zero-interest top-up loans or preferential offers to build loyalty with this client base.

Negotiating Your Mortgage Rate in 2025: How to Optimize Your Application

To secure the best possible mortgage rate, several levers can be activated:

- Play the competition: request quotes from multiple lenders and compare offers. A broker can help you save several basis points.

- Present a solid application: offer a significant down payment and submit a complete file (updated payslips, tax returns, appendices) proving a stable professional situation.

- Highlight the energy efficiency of the property: some banks offer a 0.25-point discount for homes rated A or B on the energy performance certificate (EPC).

- Leverage your savings: a proven financial buffer reassures lenders and can reduce your rate by 0.10 to 0.15 points.

- Stay loyal to your bank: existing clients may get additional discounts through partnerships with real estate advisors or brokers.

These strategies may help you break the symbolic 3% barrier on a 20-year loan—or even reach rates around 2.85% on a 15-year term, as still seen for strong profiles in July 2025.

Mortgage Rates in July 2025: Should You Borrow Now or Wait?

Deciding to buy in July 2025 depends on your priorities: take advantage of current conditions or wait for a possible rate drop at the risk of rising property prices? Buying a primary residence or investing in rental property? Given the international uncertainty, it may be wiser to act now while borrowing conditions remain favorable.

Why Borrowing in July 2025 Remains a Strategic Move

With mortgage rates stabilized around 3% for standard terms, July remains an opportune time to carry out your purchase—be it a house, apartment, plot of land, or estate. The current inertia helps prevent potential future hikes should macroeconomic conditions worsen. Moreover, summer activity levels may lead to less market competition, making your timing even better.

2025 Mortgage Rates: Wait or Take Action?

Some experts foresee additional rate cuts by the end of 2025 due to the ECB’s accommodative policy—but who can say for sure? A resurgence of inflation, rising geopolitical tensions, or another increase in the 10-year OAT could quickly reverse the trend. The risk? Delaying your purchase and losing purchasing power if property prices rise again. If you have a clear and confirmed real estate project, it's better to move forward after careful consideration.

Bonus: The 2025 Zero-Interest Loan (PTZ) – Expanded Conditions to Support Your Purchase!

Since April 1, 2025, the Zero-Interest Loan (PTZ) has been significantly simplified and expanded to support home ownership:

More Inclusive Access and Broader Geographic Scope

The PTZ is now available throughout the country, with no zoning restrictions. It applies to new properties (apartments or houses) and, under conditions, to older properties requiring renovation (at least 25% of the total cost), allowing more buyers to access advantageous financing.

Amounts and Terms Tailored to Buyer Profiles

- For a new house, the PTZ can cover up to 30% of the purchase price.

- For a new apartment, coverage ranges from 20% to 50% depending on the location, with a cap of up to €180,000.

- The repayment term may range from 20 to 25 years, with a deferred period of 5 to 15 years depending on income—offering flexibility to adjust monthly payments to your borrowing capacity.

Reinforced Yet Accessible Conditions

Eligible applicants include:

- First-time buyers (not owning property within the past two years)

- Households that meet income limits

- Buyers of a new or renovation-ready older home

The PTZ comes with no administrative fees, no interest, and no borrower insurance, which lowers the total project cost and strengthens your effective down payment.

A Powerful Complementary Tool

Used alongside a conventional fixed-rate mortgage, the PTZ reduces both the amount of the main loan and the Annual Percentage Rate (APR). It’s a real opportunity to combine financial optimization with home ownership, benefiting from competitive rates and a lower average monthly payment for your real estate project.

A Capifrance Advisor to Help Bring Your Real Estate Project to Life in July 2025

In July 2025, with mortgage rates fluctuating and the market under pressure, working with a Capifrance advisor offers a strategic advantage to succeed in buying or selling a property. Thanks to their expertise, Capifrance advisors secure every step of your transaction and maximize your chances of success.

Personalized Guidance to Buy or Sell at the Right Time

Are you a buyer? A seller? Capifrance advisors support individuals and professionals at every stage of their real estate journey: from property valuation to signing at the notary’s office, including listing optimization and negotiation. With in-depth knowledge of the local market and professional tools (virtual tours, HD photos, wide-reaching listings), they help sell your property at the right price—or identify the best purchase opportunities aligned with your budget.

Broker Partners to Help You Borrow at Competitive Rates

For buyers, Capifrance advisors can connect you with their network of mortgage broker partners—financing experts in your geographic area. These professionals help you with:

- Preparing your loan application

- Negotiating the best possible rates

- Choosing the right borrower insurance with competitive interest rates

- Optimizing your borrowing capacity

Want to strengthen your financing application? With this support, you’re well-positioned to secure a competitive mortgage rate and a reasonable debt-to-income ratio—even in a fluctuating market.

Conclusion: Key Takeaways on Mortgage Rates in July 2025

- Mortgage rates remain generally stable compared to June, with average rates ranging from around 3.05% to 3.28% depending on the loan term.

- The best borrower profiles can still secure negotiated rates below 3%.

- The ECB’s key interest rate cut to 2% in June 2025 could encourage a gradual easing of rates in the coming months.

- The market remains dynamic, notably due to price stability and a rebound in transactions.

- It is a good time to start your real estate project, with proper guidance and optimized financing.

FAQ on Mortgage Rates in July 2025

What is the current mortgage rate?

The average rate is 3.05% over 10 years, 3.04% over 15 years, 3.18% over 20 years, and 3.28% over 25 years, according to CAFPI in July 2025.

Will mortgage rates decrease in 2025?

They may stabilize or slightly decrease by the end of 2025 if the ECB continues to lower rates and inflation remains contained.

What is the monthly payment for €140,000 over 25 years?

Approximately €730 per month excluding insurance, based on a 3.20% rate.

What is the current mortgage insurance rate?

The average borrower insurance rate ranges between 0.20% and 0.40%, depending on the profile and insurance company.

What are the conditions for the zero-interest loan (PTZ)?

The 2025 PTZ is available throughout France for first-time buyers, subject to income limits and applicable for the purchase of new properties or older homes requiring renovation.

Author

Frédéric Rémy - Director of Commercial Performance

A professional in the real estate sector for several years within the Capifrance network, I would like to share with you essential advice to help you succeed in your real estate project with our advisors.